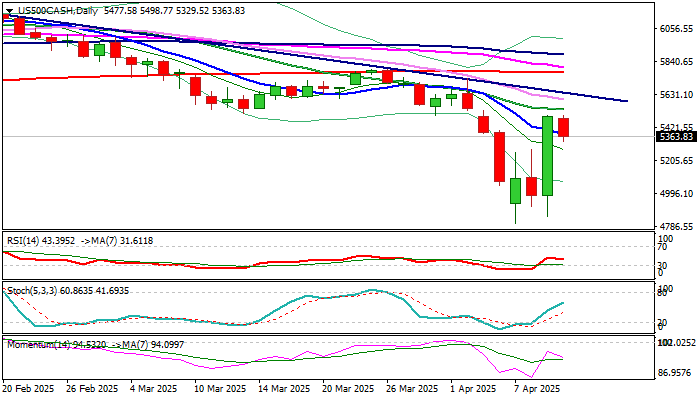

The S&P surged significantly following the U-turn in tariff policy, but further upside progress is required to offset the downside risks

The S&P 500 edged lower on Thursday after a significant 10.2% rally the previous day, marking its largest daily gain in over a decade.

President Trump’s unexpected decision to delay heavy tariffs on several countries for 90 days sparked optimism and boosted stock markets. While the fresh rally reversed much of the losses caused by tariff announcements last week, concerns remain as the US tariffs on imports from China were not impacted by the decision and were instead raised to 125%.

This development raises fears of a further escalation in the trade conflict between the world’s two largest economies, which could have a ripple effect on global markets.

The situation will be closely monitored, with a positive outcome possibly leading to a trade deal between the two nations, offering relief and lifting stock prices. On the other hand, any escalation could dampen sentiment and exert additional pressure on market prices.

Although daily indicators have shown some improvement following Wednesday’s rally, the overall outlook remains predominantly bearish, signaling that downside risks persist.

In an ideal scenario, any corrective dips from Wednesday’s peak should remain shallow and stay above the 5230 mark (Fibonacci 38.2% retracement of $4801/$5495) to maintain a healthy correction and keep the near-term bias positive for bulls. However, a sustained break above the $5500 level would be necessary to confirm a reversal.

Caution is advised if the market dips and closes below the 5200/5150 zone, as this could sideline the bullish momentum and reignite downside risks.

Res: 5457; 5496; 5532; 5636

Sup: 5330; 5267; 5230; 5200