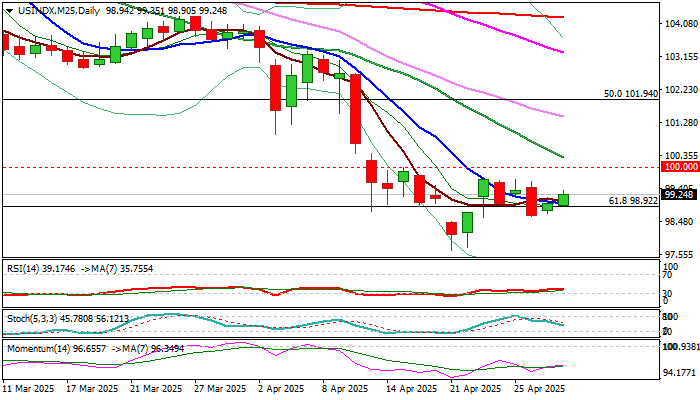

The Dollar Index is heading for its largest monthly decline since November 2022

The Dollar Index remained mildly bid on Wednesday, edging higher after data showed the U.S. economy contracted in the first quarter—contrary to expectations for modest growth—though results came in better than some major U.S. banks had projected.

Despite the uptick, the greenback remains firmly negative in the broader context, suggesting the larger bearish cycle is still intact. The recent rebound appears corrective, as conflicting signals around the US-China trade situation—whether de-escalation or renewed tensions—continue to cloud the outlook.

The Dollar Index is poised for a third straight monthly decline, with the steep downtrend from its February peak accelerating in April. This month’s slide marks the sharpest monthly loss since November 2022.

A monthly close below the key psychological 100 level would reinforce the bearish bias. However, a decisive break below the 2023/24 range floor at 99.20 is still needed to confirm the downside extension, which would then expose the next major support at 96.30 (rising trendline from the 2011 low).

Bearish daily indicators support the view of limited corrective strength, with resistance likely to cap rebounds around the 100.00/100.30 area (psychological / falling 20DMA). Further gains should be contained below the daily Kijun-sen at 100.98 to preserve the broader bearish outlook.

Res: 99.72; 100.00; 100.30; 100.98

Sup: 98.63; 97.65; 96.30; 95.18