The dollar continues to trend higher, supported by improved sentiment following the US-EU trade deal

The dollar index maintained a strong tone on Tuesday, climbing to a fresh five-week high and extending Monday’s sharp 1.1% gain—the largest one-day rise since May 12.

The greenback surged after the U.S. and European Union reached a trade agreement seen as highly favorable to the U.S. and detrimental to the Eurozone, as reflected in disappointed remarks from senior EU officials.

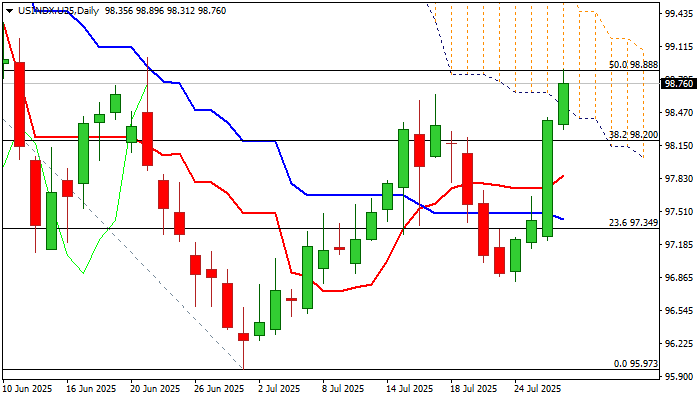

The rally saw the dollar break through the base of the descending daily Ichimoku cloud (at 98.53) and reach \$98.88, aligning with the 50% Fibonacci retracement of the \$101.80–\$95.97 decline.

Fresh momentum pushed the index above the prior recovery high of \$98.65. A close above this level would confirm a bullish failure swing pattern on the daily chart, reinforcing the positive outlook.

The daily Tenkan-sen has crossed above the Kijun-sen with growing divergence, and bullish momentum continues to strengthen. However, overbought conditions on the stochastic oscillator may temporarily slow progress near the key \$99.00 resistance area. A break above this zone would target the next significant levels at \$99.46/57 (daily cloud top / 61.8% Fibonacci retracement).

The broken cloud base now acts as solid support and is expected to limit any pullbacks.

Markets are now focused on the Federal Reserve’s upcoming interest rate decision and any forward guidance on monetary policy, as well as the final piece of key U.S. labor data—the nonfarm payrolls report (due Friday).

Today’s JOLTS report showed a notable decline in job openings for June. Traders will closely watch Wednesday’s ADP private-sector employment report for additional labor market insights.

Res: 98.88; 99.01; 99.35; 99.57

Sup: 98.53; 98.20; 97.86; 97.43